Understanding Your Paycheck: the thing that gives you the money

- Zach Zwillinger

- Jun 24

- 6 min read

Welcome to the third post of The Invested Counsel—thoughts about financial planning for young lawyers.

Understanding Your Paycheck

It is easy to ignore your paycheck. If you haven’t studied it before, it can be inscrutable. It is not organized in a linear fashion. It uses abbreviations and terms that you may not be familiar with. The math is not always obvious. And because of direct deposit, you probably never look at it.

But it’s important because it is how you get your money. And it tells a story with a beginning, a middle, and an end, and it touches on many things you need to know about your money. You can’t really understand your money without understanding where it comes from in the first place. And the guide to where it comes from is your paycheck.

So I’m going to walk through a paycheck, step by step, and explain what everything means and why it matters. I’m going to use one that I received in October 2014, when I was a third-year litigation associate at Cravath. While the tax numbers change over time, the basics generally stay the same.

Here it is:

STEP 1: GROSS INCOME – WHAT MILBANK SAYS YOU GET

You start with your salary. In 2014, I made $185,000 per year. At the end of that year, I received a $40,000 bonus; thus it is not reflected in this paycheck.

To get your total gross income for your paycheck, you take your salary, and divide it by 24 (if you get paid twice a month) or 26 (if you get paid every two weeks). At Cravath, I got a paycheck every two weeks, so $185,000 / 26 = $7,115.38.

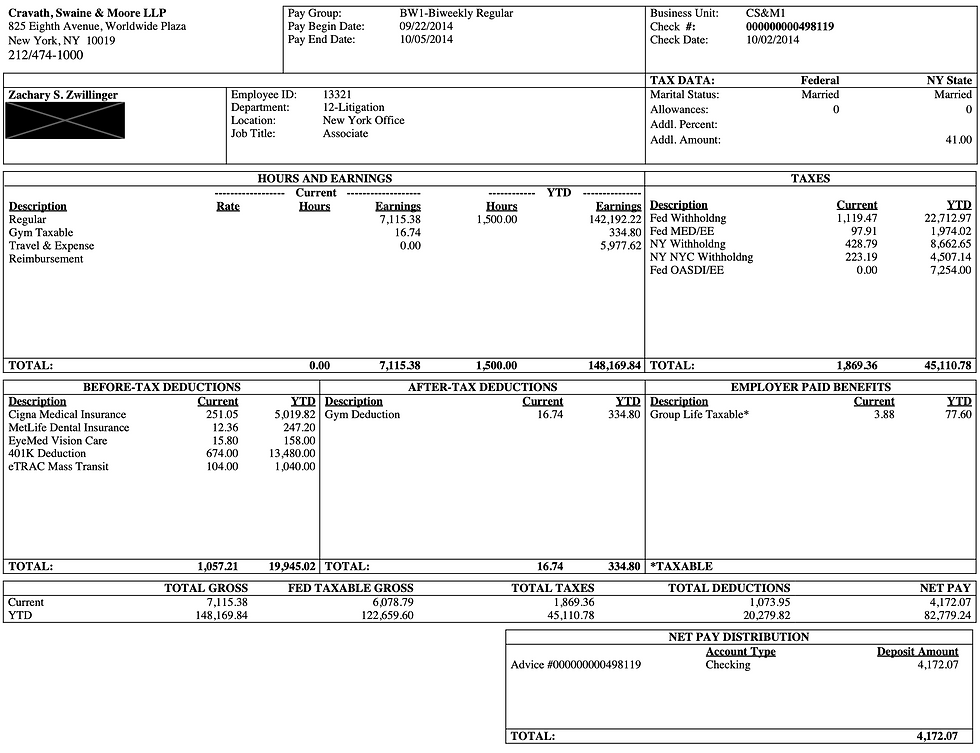

STEP 2: BEFORE-TAX DEDUCTIONS

The next step to reduce the portion of your gross income that is subject to taxes. This is done through what this paycheck calls “before-tax deductions.” These are things that you pay for with money before it is taxed. As a result, you don’t get taxed on those amounts, essentially giving you a discount to the extent of your overall tax rate. If you can pay for things with “pre-tax” or “before tax” money, that is always better.

In this paycheck, I paid for three types of insurance with pre-tax money: medical insurance, dental insurance, and vision insurance. I also made a contribution to my 401(k) retirement savings account with pre-tax money. (Importantly, amounts you contribute to your 401(k) with pre-tax money are not tax-free forever. They will be taxed in the future as ordinary income, when you take the money out.). Finally, I made a contribution to a commuter benefit card, which allows you to pay for subway fares, parking, and similar expenses with pre-tax money. If you can set this up, it’s a nice discount that doesn't take too much time.

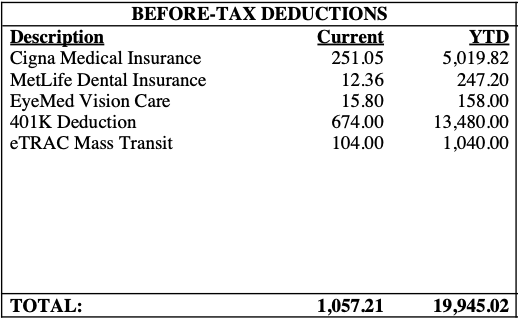

STEP 3: EMPLOYER-PAID BENEFITS

Some benefits are paid for by the firm, and so they don’t come out of your paycheck. However, the government has decided that those benefits are a form of income that should be taxed. As a result, some benefits are taxed even if you don’t pay for them. In this paycheck, Cravath paid $3.88 in benefits for group life insurance for me. Thus I’m taxed on those benefits.

These sort of benefits fall somewhere in the middle. It’s better for benefits paid by the firm to be tax free, but it’s better to pay the taxes on a benefit instead of paying for the benefit entirely out of pocket.

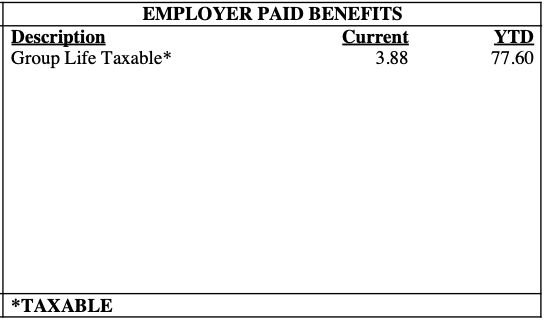

STEP 4: AFTER-TAX DEDUCTIONS

In order to get absolutely shredded, I also paid for a gym membership with my paycheck. This was through a program that the firm had with a gym, which provided a discount for signing up with that gym. Because this was not a benefit that could be paid for with pre-tax money, it was paid with after-tax money. There was no tax benefit in paying for the gym membership this way.

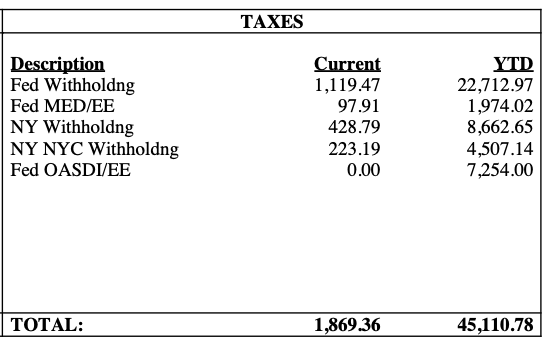

STEP 5: TAXES

After taking out all pre-tax expenses, you are left with the portion of your income that is subject to taxes. An estimation of the taxes you owe is taken out of every paycheck. These are called "withholdings." Note that they are just an estimate, and you may need to pay more or less in taxes at the end of the year, once you figure out your final tax bill.

For the purposes of this post, I’m going to assume that the taxes I actually paid were the same as the taxes withheld. It would be a pain for me to cross-reference my withholdings against my actual 2014 tax return, and I don’t feel like doing that. Also, the withholdings are often good enough; however, you should watch out if you are getting a very big tax refund each year, or if you owe any taxes each year.

There are two main categories of taxes that are taken out of your paycheck: income taxes and payroll (also known as FICA) taxes. These taxes are based on a percentage of your paycheck. Income taxes are “progressive,” meaning that the more you earn, the more you pay in income taxes per additional dollar earned. Payroll taxes are different.

Federal Income Tax. Everyone pays federal income taxes. For me in 2014, about 18% of my paycheck was withheld for federal income taxes ($1119).

State and Local Income Tax. Because I lived, and currently live, in New York City, I also pay state and local income taxes. Forty-two states impose state-level income taxes; eight do not. Notably, Texas and Florida do not impose any state income taxes. In 2014, I paid about 7% of my paycheck to New York State income taxes ($429).

In addition, New York City imposes a local income tax. Some cities do, but many do not. In 2014, I paid about 4% in New York City income taxes.

Thus for the privilege of living in New York City, I paid about 11% of my income (maybe $20,000) in taxes. This is a big expenditure. For my wife and I (in 2014), and for my family (now), living in New York City is worth it. Whether it’s worth it to you depends on you, but at the very least you should be aware of the costs when thinking things through.

Payroll (FICA) Taxes. In addition to income taxes, wages (i.e., the money that you earn from your job) are subject to payroll taxes. Payroll taxes are also known as “FICA” taxes, which stands for Federal Insurance Contributions Act. Payroll taxes go to the federal government for specific purposes.

Payroll taxes are actually paid by both the employer and the employee. The total tax rate for payroll taxes is 15.3%, with 7.65% being paid by your firm, and 7.65% being paid by you. That’s why my paycheck indicates the “EE” (meaning "employEE") next to the two categories of payroll taxes—these line items show only what I paid, not what Cravath paid.

Social Security (Fed OASDI/EE). The main portion of payroll taxes go to Social Security, which is also known as OASDI (Old-Age, Survivors, and Disability Insurance). Social Security is the federal program that (among other things, but most importantly) pays money to workers when they retire.

You pay 6.2% in Social Security taxes, but only on a portion of your income. Every year the IRS sets a “wage base limit,” which is how much of your income is subject to the 6.2% in Social Security taxes. In 2014, the Social Security wage base was $117,000. What that means is that at the start of the year, before I hit $117,000, I paid 6.2% in Social Security taxes on my paycheck. However, once I made more than $117,000 (which happened before this particular paycheck), I no longer had to pay Social Security taxes for the rest of the year. That’s why my paycheck lists $0 for how much I paid in Social Security taxes out of this paycheck.

Medicare (Fed MED/EE). The remainder of payroll taxes goes to Medicare, which is the federal program that pays for medical insurance for people over 65, as well as certain younger people with disabilities. (Don’t confuse Medicare with Medicaid; Medicare is (mostly) for older people, while Medicaid is for low-income people.) You pay 1.45% towards Medicare each paycheck. Unlike Social Security, Medicare taxes are not subject to the Social Security wage base; you pay that 1.45% on all wages, no matter how much you earn.

STEP 6: WHAT YOU ACTUALLY GET

After taking the taxes ($1,869) and deductions ($1,074) from my gross salary ($7115), I was left with $4172, or about 59% of my gross salary. About 26% went to taxes, and about 15% went to other deductions (mostly 401k contribution and health insurance). If this had been a paycheck from earlier in the year, I would have also been paying an additional 6.2% to Social Security.

In 2014, the vast majority of this paycheck went to paying for my apartment, and paying down student loans. The rest probably went to doughnuts bought at 2am from the 7-11 near my apartment.

ON ONLY GETTING HALF OF YOUR MONEY

As this shows, for most of 2014, I only received about half of my paycheck in my bank account. The first time you realize this, you get annoyed. I know I was. But that's the deal.

And it is generally better to pay for things before getting your paycheck than after, since that is how you can avoid paying taxes on some of your paycheck. Trying to avoid paying taxes is an important financial planning strategy that pops up in a lot of areas. It starts here, on your paycheck.

***

The Invested Counsel is now on Substack. If you would like to subscribe and get an emailed version of each post sent to you, go to https://substack.com/@theinvestedcounsel and sign up.

That’s all for now. Have a wonderful week.